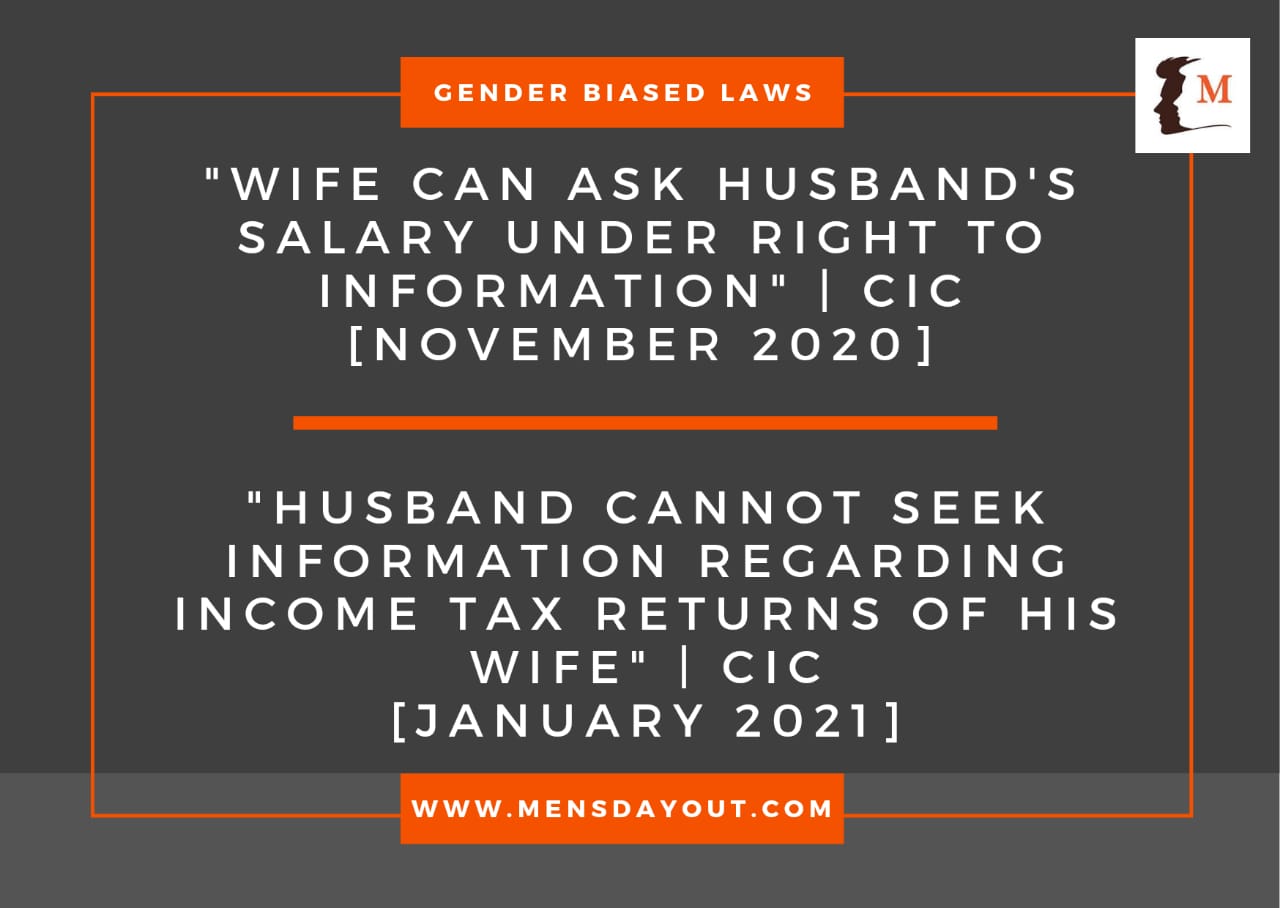

In its recent order dated January 5, 2021, the Central Information Commission (CIC) said,

Husband is not entitled to seek information regarding bank details & income tax returns of his wife under the Right to Information Act, 2005.

The Information Commissioner Neeraj Kumar Gupta observed that the filing of the Income Tax Returns by an individual with the Income Tax Department is not a public activity. The commission said,

It is in the nature of an obligation which a citizen owes to the State viz. to pay his taxes, this information cannot be disclosed to the applicant in the absence of any larger public interest.

Case:

Appellant Husband wanted the information related to name and branch address of all those banks wherein his spouse was having account, at any point of time, during the financial years 2012-2013 to 2017-2018.

As reported by LiveLaw, appellant contended before the Commission that he was seeking information about his legally wedded wife, and therefore, the CPIO should have invoked Section 11 of the RTI Act, 2005.

Further, he submitted that the information regarding her bank details & income tax returns should be disclosed.

CIC Response

The respondent (CPIO, O/o. the Income Tax) submitted that the appellant was seeking clarification with regard to the bank details & income tax returns of his wife, which is personal in nature and therefore CPIO, O/o. the Income Tax claimed exemption u/Section 8(1)(j) of the RTI Act, 2005.

It was also submitted that Section 11 of the RTI Act, 2005 can only be invoked if the CPIO intends to disclose the personal information and therefore, once the CPIO is satisfied that the information is to be denied under Section 8(1)(j) of the RTI Act, 2005, Section 11 is not required to be invoked.

Lastly, the respondent stated that prima facie, no larger public interest is involved in the matter and hence, the CPIO did not intend to disclose this information.

Decision of the Commission

The Commission greed with the stand of the respondent in not invoking Section 11 of RTI Act and said,

The CPIO is expected to follow the procedure of Section 11 when he ‘intends to disclose any information or record’. In the present case, the CPIO did not find any merit in disclosure and accordingly, Section 11 was not invoked.

Further, with regards to the applicability of Section 8(1)(j) of the RTI Act, 2005 for non-disclosure of the third party bank details and income tax returns, the Commission referred to the Supreme Court’s Judgment in the case of Girish Ramchandra Deshpande v. Central Information Commission [(2013) 1 SCC 212].

In the above said case, the supreme court had ruled the details disclosed by a person in his income tax returns are “personal information” which stand exempted from disclosure under clause (j) of Section 8(1) of the RTI Act, unless involves a larger public interest and the Central Public Information Officer or the State Public Information Officer or the Appellate Authority is satisfied that the larger public interest justifies the disclosure of such information.

The Commission also referred to the Delhi High Court judgment in Vijay Prakash v. Union of India [AIR 2010 Delhi 7] in which it was held that, in a private dispute between husband and wife, the basic protection afforded by virtue of the exemption from disclosure enacted under Section 8(1)(j) cannot be lifted or disturbed unless the petitioner is able to justify how such disclosure would be in ‘public interest’.

The Court also noted the definition of ‘Third Party’ and observed that the husband in this case is a ‘third party’ for the purpose of the RTI Act. The court stated,

From the words circumscribed u/Section 2(n) of the RTI Act, 2005, it is vividly clear that any person other than the citizen making a request for information can be termed as ‘third party’. Therefore, Ms. Mamta @ Mamta Arora being a person other than the RTI applicant surely comes within the definition of ‘third party’.

Moreover, the CPIO has also not intended to disclose the information treating it as confidential and has rather pleaded that there is no public interest in the matter. This Commission also does not find any public interest which outweighs the harm caused in its disclosure.

Lastly, the Commission, after considering the factual matrix of the case was of the opinion that in the absence of any larger public interest in the matter, the appellant is not entitled to seek information regarding bank details & income tax returns of his wife which is exempted u/Section 8(1)(j) of the RTI Act, 2005.

With the above observations, the appeal was disposed of.

CLICK ON THE LINK TO READ FULL ORDER

Wife Can Seek Details

In a sharp contrast to the above order, in November 2020, the Central Information Commission partly allowed a wife’s appeal, seeking information about her husband’s income under the Right to Information Act, 2005.

Information Commissioner Neeraj Kumar Gupta, while relying on certain High Court orders where it was held that a wife is entitled to know what remuneration her husband is getting, directed the Income Tax Authority to provide the Appellant with ‘generic details’ of the net income of her husband.

The Commission relied on a ruling of the Madhya Pradesh High Court in Sunita Jain v. Pawan Kumar Jain & Ors., where it was opined thus:

While dealing with the Section 8(1)(j) of the Act, we cannot lose sight of the fact that the appellant and the respondent No. 1 are husband and wife and as a wife she is entitled to know what remuneration the respondent No. 1 is getting.

In doing so, the High Court had distinguished from the case of Girish Ramchandra Deshpande v. CIC & Ors., whereby the Supreme Court had pronounced that details disclosed by a person in his income tax returns are “personal information” which stand exempted from disclosure under clause (j) of Section 8(1) of the RTI Act, unless involves a larger public interest.

Reference was also made to a decision of the Nagpur Bench of the Bombay High Court in Rajesh Ramachandra Kidile v. Maharashtra SIC & Ors., where while denying information about the income of an individual to a complete stranger, the Court had remarked,

In a litigation, where the issue involved is of maintenance of wife, the information relating to the salary details no longer remain confined to the category of personal information concerning both husband and wife, which is available with the husband hence accessible by the wife.

In view thereof, the Commission then ordered:

The Commission directs the respondent to inform the appellant about the generic details of the net taxable income/gross income of her husband held and available with the Public Authority for the period 2017-2018, within a period of 15 working days.

The Commission however denied Appellant’s request seeking photocopies of income-tax returns filed by her husband. It held,

The information sought by the appellant regarding copies of income tax returns of her husband, etc. is personal information of third party, which cannot be disclosed under Section 8(1)(j) of the RTI Act.

CLICK ON THE LINK TO READ FULL ORDER

ALSO READ –

http://voiceformenindia.com/in-the-news/child-custody-to-fathers-in-india/

http://voiceformenindia.com/in-the-law/bank-fined-for-sharing-account-statements-with-wife/

http://voiceformenindia.com/in-the-law/new-supreme-court-guidelines-on-maintenance/

http://voiceformenindia.com/in-the-law/courts-could-even-consider-appointment-of-a-local-commissioner-to-assess-the-standard-of-living-of-husband/

We are now on Telegram. You can also join us on our Facebook Group

Join our Facebook Group or follow us on social media by clicking on the icons below

If you find value in our work, you may choose to donate to Voice For Men Foundation via Milaap OR via UPI: voiceformenindia@hdfcbank (80G tax exemption applicable)

Follow Us

{kind=link}